Daily Comment – Dollar stands tall after robust jobs report

- Strong US data dent chances of a 50bps Fed rate cut

- Plethora of Fed speakers on the wires today

- Dollar enjoys strong gains, stocks rally unexpectedly

- Oil pushes higher as gold’s retreat continues

US jobs report surprises to the upside, doves are displeased

Another exciting week commences as market participants are still digesting the unexpectedly strong US labour market data. The plethora of upside surprises has crushed the chances of another 50bps rate cut at the November 7 meeting, with even the doves acknowledging the fact that the US economy is confidently growing.

The plethora of upside surprises has crashed the chances of another 50bps rate cut at the November 7 meeting

We are likely to hear more on this issue this week, as more than 10 Fed members will be on wires, starting with Kashkari, Bostic, Musalem and Bowman today. Apart from the doves, who will try to manage expectations after the strong US data, it will be interesting to see how the hawks handle the situation in terms of the need for another rate cut in November. Interestingly, the debate could become even more complicated if Thursday’s September CPI report produces another upside surprise.

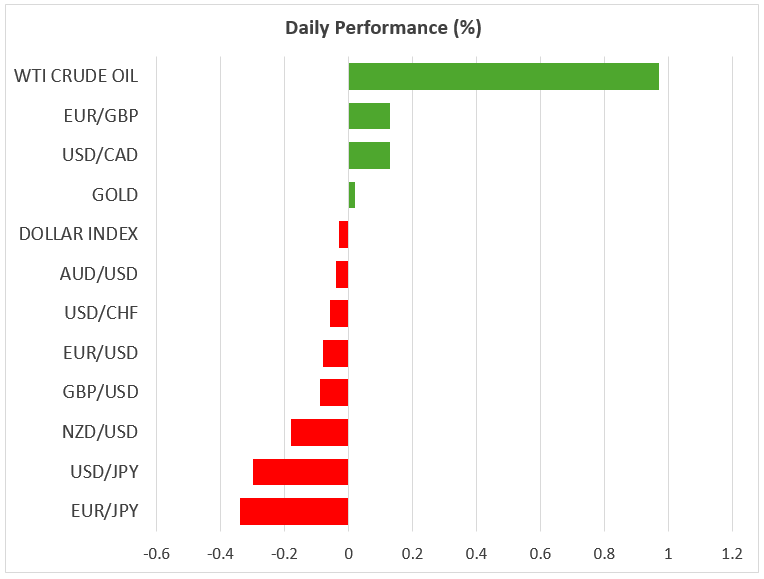

Dollar enjoys a strong weekly performance

The US dollar was the main beneficiary of last Friday’s data, as the dollar index recorded its strongest weekly performance since September 23, 2022, led by the correction in euro/dollar, which at the time of writing is hovering below the key 1.1000 level, and with dollar/yen climbing abruptly above 148.00.

While the dollar’s reaction was largely expected, the equities’ move produced some question marks. Up to now, the positive market momentum was fueled by the expectations that the Fed will continue to ease its monetary policy stance. However, equities traded higher as if the market shifted gear and was more interested and content with the underlying strength of the US economy.

Equities traded higher as if the market shifted gear and was more content with the underlying strength of the US economy.

This reaction was even more intriguing as the newsflow from the Middle East remained negative. Disappointingly over the weekend, both Israel and Iran’s proxies continued their barrage of attacks, and there is no end in sight. Today marks the one-year anniversary of Hamas’ brutal attack inside Israel. With Israel still pondering its response to last week’s direct Iranian attack, which could even involve targeting Iran's nuclear facilities, negotiations for a temporary ceasefire or a solution have broken down.

Pressure from President Biden for some sort of agreement will continue, as such an outcome might also boost Harris’ electoral chances. Indeed, we have entered that last stretch, as there are fewer than 30 days left before the election, which means the rhetoric from both sides is expected to become more aggressive.

Pressure from President Biden for some sort of agreement will continue, as such an outcome might also boost Harris’ electoral chances

Oil trades higher, gold affected by the stronger dollar

Oil continues its journey higher, temporarily surpassing the $76 level, and thus trading around 13% higher from its early-September lows. This bullish move might have legs, as energy, oil and gas installations are high on the target list for both sides in the Middle East conflict.

On the flip side, the improved risk sentiment and the dollar’s gains have pushed gold below the $2,650 area. This is the fourth consecutive red daily session for gold, but a more protracted correction needs sustainably good US data and a barrage of positive news regarding the Israel-Iran conflict.

Related Assets

Latest News

Disclaimer: The XM Group entities provide execution-only service and access to our Online Trading Facility, permitting a person to view and/or use the content available on or via the website, is not intended to change or expand on this, nor does it change or expand on this. Such access and use are always subject to: (i) Terms and Conditions; (ii) Risk Warnings; and (iii) Full Disclaimer. Such content is therefore provided as no more than general information. Particularly, please be aware that the contents of our Online Trading Facility are neither a solicitation, nor an offer to enter any transactions on the financial markets. Trading on any financial market involves a significant level of risk to your capital.

All material published on our Online Trading Facility is intended for educational/informational purposes only, and does not contain – nor should it be considered as containing – financial, investment tax or trading advice and recommendations; or a record of our trading prices; or an offer of, or solicitation for, a transaction in any financial instruments; or unsolicited financial promotions to you.

Any third-party content, as well as content prepared by XM, such as: opinions, news, research, analyses, prices and other information or links to third-party sites contained on this website are provided on an “as-is” basis, as general market commentary, and do not constitute investment advice. To the extent that any content is construed as investment research, you must note and accept that the content was not intended to and has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such, it would be considered as marketing communication under the relevant laws and regulations. Please ensure that you have read and understood our Notification on Non-Independent Investment. Research and Risk Warning concerning the foregoing information, which can be accessed here.